What a mess!

The results we are currently seeing in portfolios managed by banks and wealth managers are frightening. One looks in vain for overall portfolios with positive returns and the differences between the best and worst returns are greater than ever. Anyone who is still hoping that things will recover quickly, as in the past few years, may be very shocked. Because the weather conditions have changed fundamentally after 30 years of falling interest rates and good growth. The old risk patterns only apply to a limited extent and inaction appears to be a bad option.

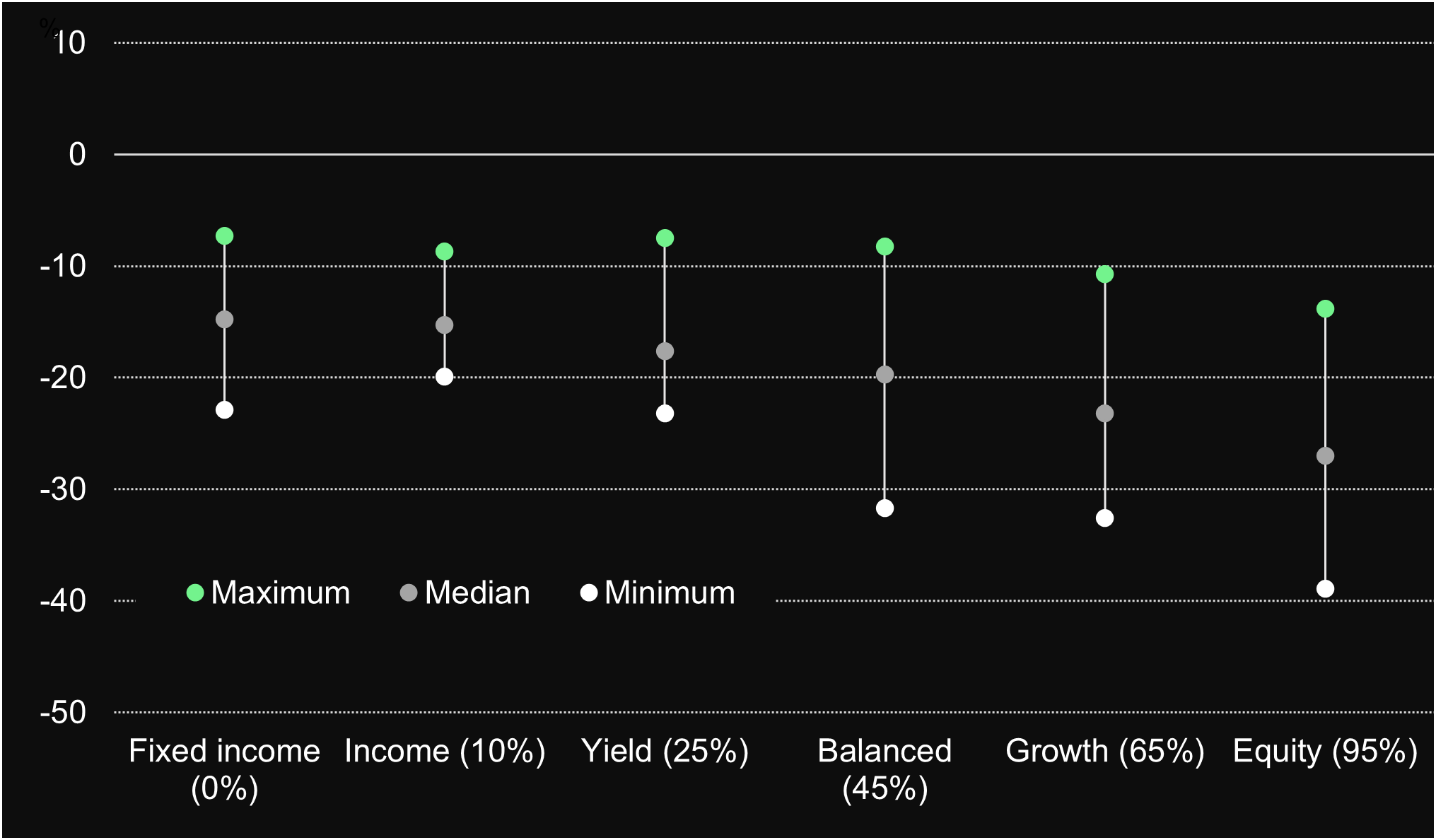

Anyone who is currently looking at their own investment portfolio needs good nerves. Performances once again deteriorated significantly in the third quarter. The charts aside provide a summary of the results and allow you to easily categorize your own portfolio returns.

Three special features that catch the eye

On average, US Dollar denominated portfolios are in a bad way, depending on the risk category, between -12.9% and -25.1%. Despite the good profits, these are very large losses and a further deterioration cannot currently be ruled out. Three aspects in particular stand out in the analy

- No positive returns: No asset manager has been able to buck the negative trend. All portfolios examined show a significant negative return for the year, regardless of risk profile and currency.

- Greater scatter than ever before: the difference between the best and the worst determined result in a risk category has never been so great since the start of the measurements in 2014. On average, the best and worst returns were 17.2 percentage points apart (as opposed to the long-term average of 12.5 percentage points). These are worlds.

- Distorted distribution of risk: But the conventional classification according to risk groups also seems to have little effect. In an inflationary environment with rising interest rates, the simplification of more stocks equals more risk no longer works to the same extent. This is reflected in the median and maximum values, which are very close to each other across all risk groups.

The difference between good and mediocre asset management has seldom been as obvious as it was this year.

Patrick Müller, CEO ZWEI Wealth

Four features that should make you suspicious

The question remains whether an adjustment to the portfolio is indicated or not. A definitive answer can only be given in individual cases. Nevertheless, the analysis indicates four features that should make you suspicious:

- No outperformance in recent years: be careful if the portfolio has not been one of the best in recent years

- Many funds: Be careful if the portfolio has a high proportion of funds

- High proportion of bonds and alternative investments: With these, the portfolio tends to be highly sensitive to interest rates

- No cost overview: Portfolios for which the cost overview is difficult and is not explicitly shown

Doing nothing is no longer a good option!

It is important to note that returns are usually only part of the problem. In many portfolios, there is a general lack of transparency, overview, an individualized strategy with a focus on goals and, of course, the costs are far too high. In a market environment that is changing fundamentally after 30 years of fundamentally falling interest rates, doing nothing seems a bad option. It is worthwhile right now to fundamentally review the portfolio and, if necessary, to reorganize it.

About the analysis ZWEI Wealth analyzes the results achieved by banks and asset managers on a quarterly basis. The analysis covers 114 institutions with a total of 378 portfolio types (varies depending on the risk category and currency). The return figures basically correspond to a net value according to the GIPS standard. |

{kind=link}